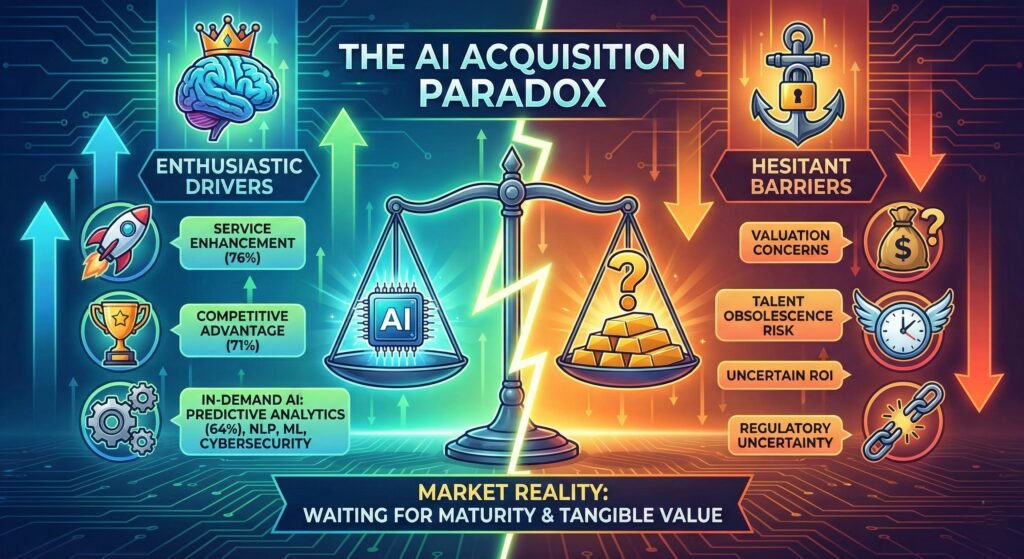

Artificial intelligence has become the most talked-about technology in boardrooms worldwide, but despite overwhelming interest, more than one-in-three buyers haven’t made a single AI-related acquisition. This paradox reveals a market caught between opportunity and uncertainty, where the promise of transformation clashes with practical concerns about value, talent, and obsolescence. What’s driving AI Acquisitions? According to a 2025 Global Buyers Report by Equiteq, Companies aren’t buying AI for cost savings—they’re chasing differentiation. The report shows 76% of corporate acquirers cite service enhancement as their primary driver, while 71% focus on competitive advantage. Private Equity firms mirror these priorities, with 70% seeking differentiation for portfolio companies. This signals a fundamental shift: AI isn’t viewed as an operational tool but as essential to staying relevant. The AI Capabilities In Demand Why The Hesitation? Where Companies Stand Today? Many companies are still establishing concrete use cases that create genuine competitive advantages. Success increasingly hinges on data infrastructure—AI models are only as effective as the data feeding them. Beyond valuation concerns, three operational challenges are slowing deal activity: (i) risk aversion around unproven technologies, (ii) lack of internal expertise to properly evaluate AI companies, and (iii) regulatory uncertainty as governments worldwide grapple with AI oversight. These areas require greater certainty before buyers commit capital to AI acquisitions. What’s Next For AI M&A The market is maturing from hype-driven speculation toward disciplined deal-making. Buyers are asking harder questions about real business problems, talent sustainability, and value justification. While current activity remains measured, acquisition momentum will build as AI technologies mature, use cases crystallize, and tangible outcomes multiply. The buyers sitting on the sidelines today aren’t disinterested—they’re waiting for clearer signals about which capabilities will deliver lasting value in an industry where patience may prove the smartest strategy.