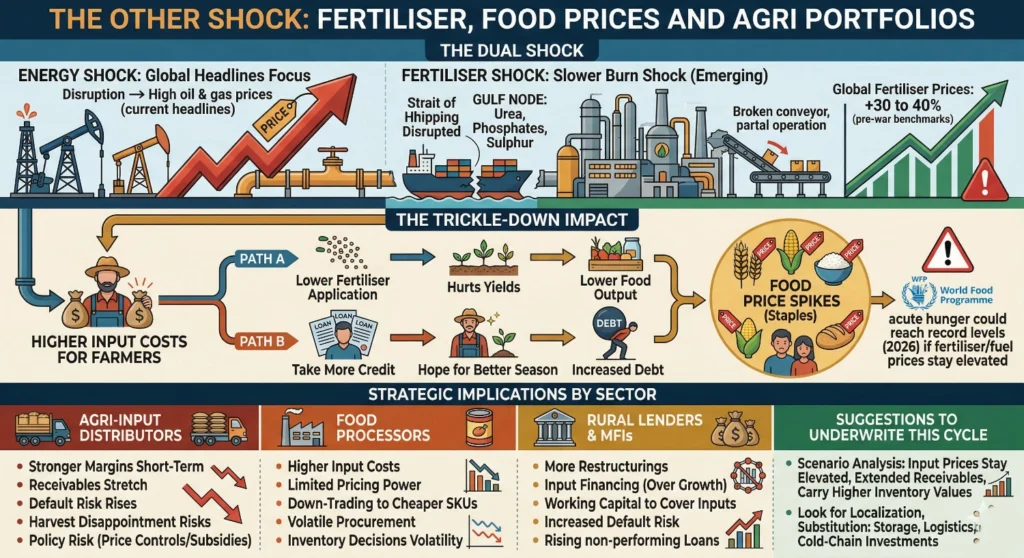

Most headlines are focused on oil and gas. But there is a second, slower burn shock building in fertilisers and food costs that matters just as much for investors with exposure to agri, food and rural consumption.

The Gulf is not only an oil and LNG exporter. It is also a major node for key fertiliser inputs and processed products. A large share of traded urea, phosphates and sulphur originates in or moves through this corridor. With the Strait of Hormuz effectively constrained, freight disrupted and plants intermittently offline, global fertiliser prices have already moved 30 to 40 percent off pre‑war levels on some benchmarks.

Potential Impact:

- Higher fertiliser prices lift input costs for farmers

- Some respond by cutting application rates, which hurts yields. Others take more credit and hope for a better season

- One crop cycle later, lower output and higher costs combine into food price spikes, especially for staples

The World Food Programme is already warning that acute hunger could reach record levels in 2026 if the conflict persists and fertiliser and fuel prices stay elevated.

What This Means For Companies or Investors – By Sector

- Agri‑input distributors may show stronger margins short term, but receivables stretch, default risk rises if harvests disappoint, and policy risk around price controls/subsidies increases

- Food processors face higher input costs, limited pricing power, down‑trading to cheaper SKUs, and more volatile procurement and inventory decisions

- Rural lenders and Micro Finance Institutions (MFIs) see more restructurings, working capital borrowing to cover inputs rather than growth

Suggestions To Underwrite This Cycle

- Build scenarios where input prices stay elevated for two to three seasons, receivable days extend and inventory needs to be carried longer at higher values

- Look for localization and substitution angles including storage, logistics and cold‑chain investments that mitigate food loss and smooth volatility