Distressed M&A: The Opportunity Most Buyers Miss

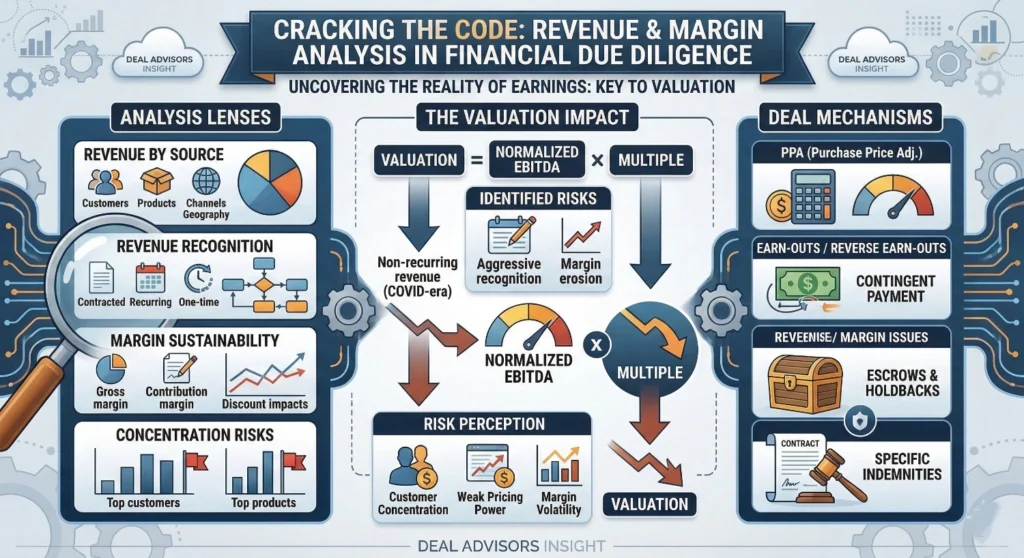

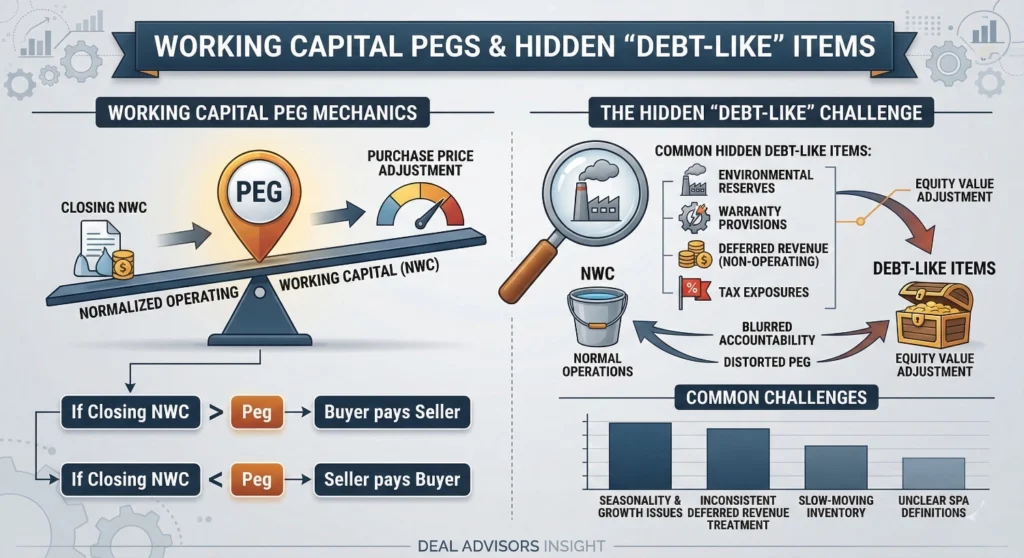

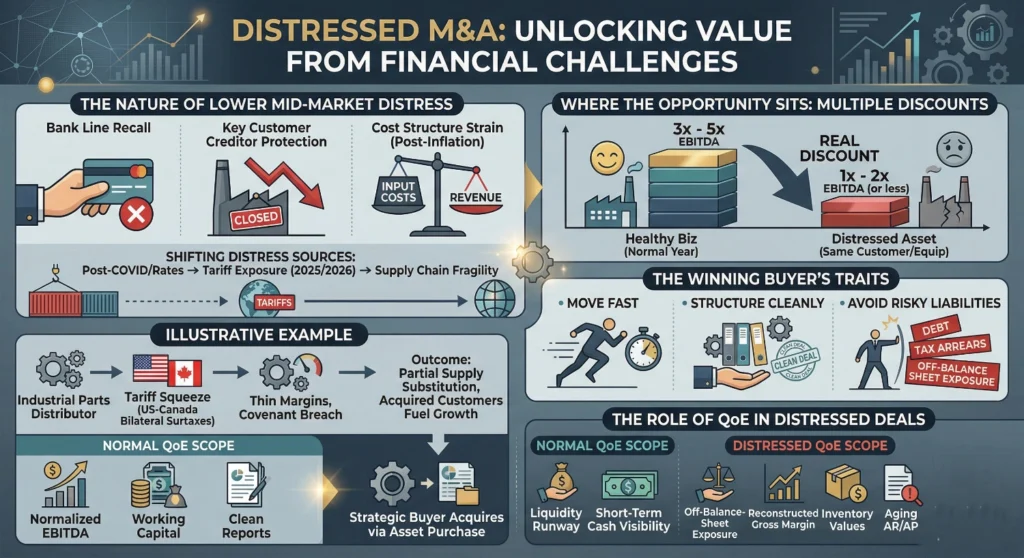

Distressed M&A means acquiring a business in financial or operational trouble. In the lower mid-market, the distress rarely arrives via a formal restructuring process. It shows up as a bank line being called, a key customer filing creditor protection, a cost structure that made sense at pre-inflation input prices but not today. The discount is real. So is the complexity. What has changed is the source of the distress. Through 2023 and 2024 it was post-COVID normalization and rate shock doing the damage. Today it is tariff exposure and supply chain fragility. Businesses in manufacturing, distribution, and industrial services that could not absorb the margin compression were the distressed targets in 2025 and for 2026. Why Lower Mid-Market Distress Is Harder Than It Looks? For businesses operating in this space, books are often in poor shape. The owner runs the business, with no management layer beneath. Customer and supplier relationships are informal. There is no restructuring / financial advisor. You are doing diligence on a company that could not afford to keep its accounting current while the clock is ticking on a landlord, a lender, or tax arrears balances. The buyer who wins here is not the one with the highest bid. It is the one who moves fast, structures cleanly, and knows what liabilities to stay away from. Where the Opportunity Sits Distressed deals trade at multiples that healthy businesses do not. A business doing $500K in EBITDA in a normal year might transact at 3x-5x in a competitive process. In distress, the same asset with the same underlying customer relationships and equipment might clear at 1x to 2x, sometimes less. The value is not in the distress itself. It is in the buyer’s ability to stabilize and normalize what the previous owner could not. Illustrative Example: A mid-size industrial parts distributor built its book around US-sourced components sold primarily into the Canadian market. When the March 2025 tariff rounds hit, the 25% US surtax on Canadian goods combined with Canada’s retaliatory measures on US imports created a bilateral squeeze. Landed costs on the distributor’s primary SKU lines increased roughly 18 to 22%. The business had thin margins to begin with and had not passed through cost increases fast enough to protect cash flow. By mid 2025, it was drawing on its revolving facility to fund operations and had breached a covenant. A strategic buyer in the same sector acquired the business through an asset purchase. Structure excluded the operating line balance and a disputed supplier payable. Purchase price came in at approximately 0.4x trailing revenue. The buyer had two things the target did not: an existing supplier relationship that partially substituted the US-sourced components and enough scale to absorb the transition period. The acquired customer relationships contributed to new contract wins within 90 days of close. Role Of QoE In a distressed lower mid-market deal, the QoE scope shifts. Liquidity runway, short-term cash visibility, and off-balance-sheet exposure take priority over a clean normalized EBITDA build. The focus is not trying to get to perfect information, but identifying what kills the deal or the business post-close. The QoE work needs to reconstruct gross margin on a normalized cost basis. It also needs to scrutinize inventory carrying values, customer receivable and supplier payable aging, and any balance sheet and off-balance-sheet exposures. Worth Discussing: If you are looking at a distressed deal, we would welcome a discussion around the QoE scope.