The US dollar is still the world’s main reserve currency, but it has become weaker and more volatile over the past year. That matters for anyone holding US assets from outside the US.

Since January 2025 it has fallen by about 10% against a broad basket of currencies, even though US growth and equity markets look strong. For foreign investors, this means a large part of the S&P 500’s 14% gain in dollar terms has been offset once returns are converted back into their home currency.

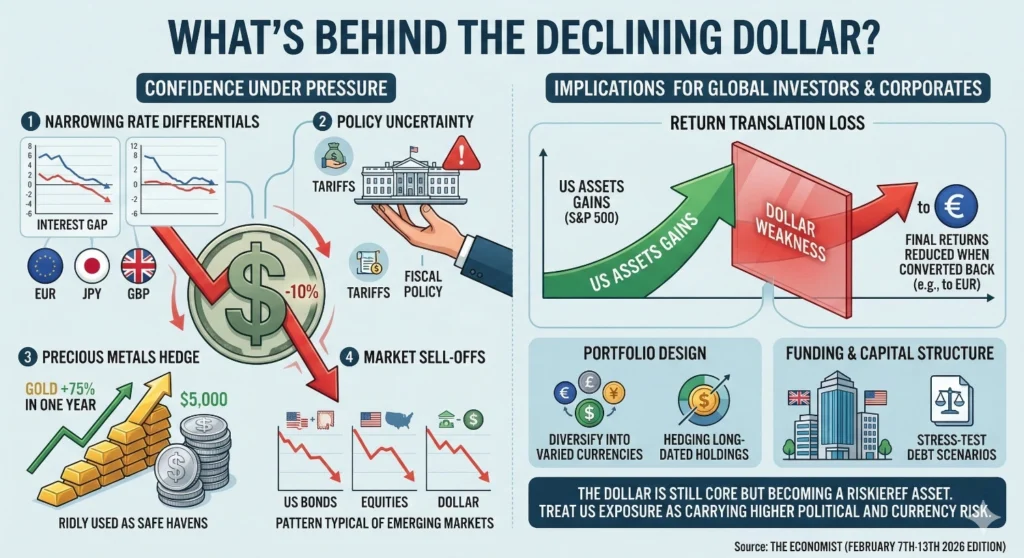

Why the dollar is under pressure?

Several factors are undermining confidence in the dollar, even though US growth and US equity markets still look strong.

- Narrowing interest‑rate differentials: The gap between US rates and other major economies has shrunk

- Policy uncertainty: Aggressive tariffs, public pressure on the Federal Reserve, and relaxed fiscal policy have made investors more nervous about US assets

- Gold and silver prices: Gold has surged to around $5,000, up by 75% in a year, while silver has seen sharp swings. Investors are using precious metals as a hedge against dollar and policy risk

- Sell‑off episodes: There have been several moments when US bonds, equities and the dollar have fallen together—a pattern more typical of emerging markets

The nomination of Kevin Warsh as the next Fed chair gave brief relief, because of his earlier hawkish reputation. But his current call for rate cuts, even with current inflation (2.8%) still above target (2%) and further fiscal stimulus coming, could add to concerns that US policy will weaken the currency over time.

Even after its recent decline, the dollar is still overvalued on most measures. At the same time, foreign investors have limited alternatives as the dollar still dominates global trade invoicing, cross‑border banking, international debt and FX transactions.

Practical implications for Global Investors and Corporates

- Return translation: Foreign investors in US assets need to factor in FX risk explicitly. Strong local‑currency returns can be largely offset by dollar weakness, as we saw last year in euro terms

- Portfolio design: It is sensible to increase currency diversification and hedging, especially for long‑dated holdings in US equities and credit

- Funding and capital structure: Multinationals that borrow in dollars but report in other currencies should stress‑test their balance sheets for a scenario of further dollar depreciation and higher volatility

In short, the dollar is still the core funding and reserve currency, but it is becoming a riskier asset. Anyone managing capital across borders should treat US exposure as carrying higher political and currency risk than in the pre‑2020 period and adjust pricing, hedging and governance expectations accordingly.

Source: The Economist (February 7th-13th 2026 edition)