In our last issue, we explored working capital pegs and debt-like items. This issue examines revenue and margin quality—the bedrock of any Quality of Earnings (QoE) analysis and the primary driver of enterprise value.

What This Means: Revenue and margin analysis evaluates not just how much a business earns, but how reliable, repeatable, and profitable those earnings really are. It dissects revenue drivers (price, volume, mix), customer and product economics, and cost structures to identify normalized earnings.

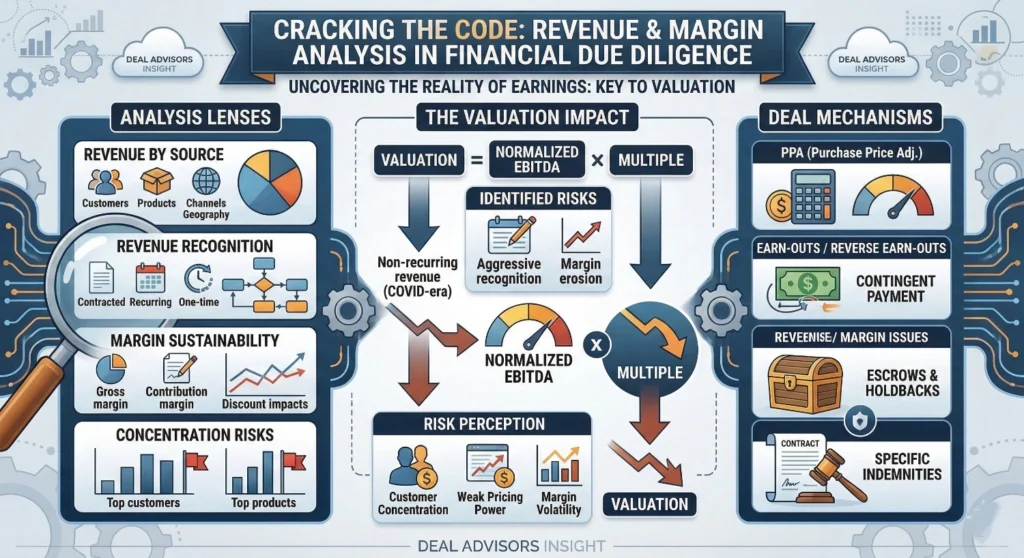

The Challenge: Reported sales growth and margins often mask underlying fragility. Common issues include:

- One-off or COVID-era spikes that inflate revenue and margins

- Aggressive revenue recognition (early cut-off, bundled contracts, “book-and-bill” practices)

- Margin erosion hidden by mix shifts, discounting, or under-accrued costs

- Poor data quality and inconsistent segment reporting, limiting insight into true drivers

Why It Matters (and How It Impacts Valuation): Valuation in deals is usually anchored on a multiple of normalized EBITDA. If revenue is less recurring than presented or margins are overstated, normalized EBITDA comes down—and every turn of the multiple compounds that value impact.

Beyond the level of EBITDA, quality of revenue and margins affects the multiple itself:

- Higher recurring, contracted, diversified revenue and stable margins support a higher multiple (lower perceived risk)

- Customer concentration, volatile margins, or weak pricing power push multiples down as investors price in higher risk and volatility

In effect, revenue and margin analysis influences both sides of the valuation equation: the normalized earnings, and the multiple (risk and sustainability).

What Does the Financial Due Diligence Analyze?: A robust due diligence systematically dissects revenue and margins through the following lenses:

- Revenue breakdown by source

- By customer, product/service, channel, geography, and contract type

- Discontinued products/services: Revenue phasing out or discontinued lines excluded from run-rate calculations to avoid overstating future performance

- Revenue recognition

- Recurring vs. non-recurring vs. one-time or project-based revenue

- Revenue recognition policies vs. applicable accounting standards and industry norms

- Margin analysis and sustainability

- Gross margin by product, customer, and channel, including trend and mix impacts

- Contribution margin by business line and impact of discounting, input costs, and FX

- Concentration and dependency

- Top customers, top products, key suppliers, and the sensitivity of margins to changes in any of these

- Pro forma and normalization

- Pro forma revenue adjustments: For recent acquisitions, new contracts, or operational changes, presented “as if” they occurred in prior periods (e.g., integrating acquired revenue streams or reflecting new product launches retroactively)

- Period-on-period bridges of revenue and EBITDA (volume, price, mix).

- Adjustments for non-recurring items, accounting policy changes, and run-rate changes to arrive at normalized EBITDA

Real Deal Context: During a sell-side due diligence for a commercial services company, our analysis revealed significant revenue and outsized margins from COVID-related supplies (hand sanitizers, disinfectants, etc.) during peak pandemic months.

We adjusted reported revenue by removing these non-recurring sales and the associated margins from the normalized run-rate, thereby presenting a credible view of underlying performance.

Deal Mechanisms to Address Revenue and Margin Issues: When revenue or margin risks are identified, common deal structuring mechanisms include:

- Purchase price adjustment (PPA)

- Upfront price reduced or adjusted via closing accounts or working capital mechanisms to reflect a lower or more volatile EBITDA base

- Earn-outs and reverse earn-outs

- Part of the consideration made contingent on achieving agreed revenue, EBITDA, or margin targets post-close

- Reverse earn-outs reduce price if performance falls short, protecting the buyer against downside

- Escrows and holdbacks

- A portion of the price is held in escrow to cover identified risks (e.g., disputed contracts, key customer renewals, or cost understatements that could hit margins)

- Specific indemnities and covenants

- Targeted indemnities for known revenue recognition issues, disputed contracts, or pricing commitments.

- Operational covenants to protect the integrity of earn-out metrics where the seller remains involved post-close

These tools allow parties to share risk around uncertain revenue and margin outcomes instead of walking away from the deal.

Are You Prepared? If you are contemplating a transaction or want a pre-diligence ‘health check’ around your business, we would be happy to discuss.