In our last issue, we covered Quality of Earnings (QoE), including a Net Working Capital example. This issue dives deeper into working capital pegs and debt-like purchase price adjustments.

What This Means: Net Working Capital (NWC) is a negotiated lever that directly influences purchase price through the working capital peg. The peg represents the normalized level of operating working capital a business needs, and is negotiated during the due diligence exercise using the most recent 12–24 months average to strip out seasonality and unusual items. Closing NWC is measured as of closing date using preliminary estimates, with final true-up adjustment 60-120 days post-close.

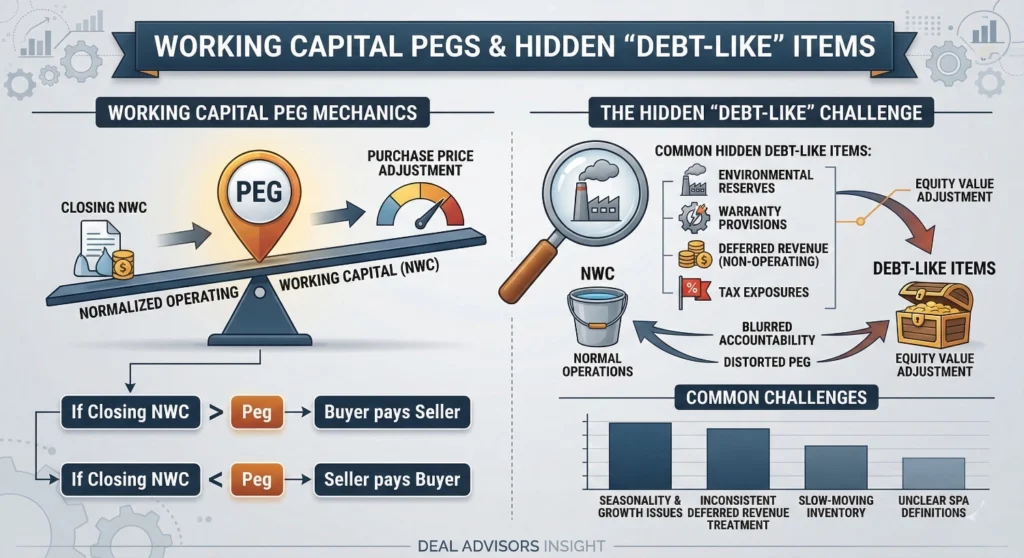

In a cash‑free, debt‑free deal, NWC is usually defined as current assets (excluding cash) minus current liabilities (excluding debt and agreed debt‑like items), and deviations from the peg at closing drive dollar‑for‑dollar price adjustments. In summary, If closing NWC < peg, seller pays buyer (decreases purchase price). If closing NWC > peg, buyer pays seller (increases purchase price).

The complexity lies in deciding what belongs in “operating” working capital versus what should be treated as debt‑like. Long‑dated or non‑operating obligations—such as environmental reserves, large warranty provisions, certain deferred revenue, or tax exposures—often behave more like debt in economic terms. If they remain inside working capital, they can distort the peg and blur accountability for future cash outflows; if reclassified as debt‑like, they reduce equity value or are settled by the seller outside the peg.

Common Challenges:

- Seasonality and growth are not properly captured, leading to pegs set off a peak or trough period rather than a representative average of business needs

- Deferred revenue, customer deposits, and prepayments are treated inconsistently across the NWC definition, the EV‑to‑equity bridge, and the purchase agreement, creating ground for post‑close disputes

- Slow‑moving inventory, obsolete stock, and inadequate reserves for bad debts overstate the quality of current assets and inflate “true” NWC, which can quietly shift value from buyer to seller.

- Changing cut‑off policies (e.g., received‑not‑invoiced, accruals) during the review period are not documented, obscuring trends in payables and accruals used to set the peg

- Generic SPA definitions of “net working capital” and “indebtedness” do not reflect how specific accounts (warranties, environmental, taxes, deferred revenue) are actually treated in the peg and debt‑like schedule

Real Deal Context: One of our clients acquired an industrial manufacturing company in a cash-free, debt-free transaction where the target carried historical environmental exposure and longer-term product warranties.

During our due diligence, we identified sizeable environmental and warranty reserves in “accrued liabilities”—treated as current liabilities and included in historical NWC. Management noted these obligations would resolve over years but argued they were part of normal operations and embedded in historical financials.

The buyer pushed to reclassify them as debt-like items for the EV-to-equity bridge. The parties agreed to:

- Restate 12 months of NWC excluding these reserves, raising the normalized NWC and supporting a higher working capital peg for true operating needs

- Add the reserves to a debt-like schedule with a downward equity adjustment

- Fund a modest escrow for potential tail risk above booked amounts.

This preserved buyer protection and seller economics without renegotiating headline value.

Suggested Success Factors:

- For buyers: Build the peg from a monthly NWC time series that reflects the final, agreed definition of working capital, explicitly separating recurring operating accruals from true debt‑like exposures in a dedicated schedule

- For sellers: Prepare a working capital memo early that explains reserves, cut‑off practices, seasonality, and any recent changes, and use it to support both the peg and the argument for what should remain in operating NWC versus become debt‑like

- For both parties: Lock definitions of net working capital, cash, and debt‑like items at LOI and mirror them in SPA exhibits; consider collars (or, pre-agreed buffers, such as, no adjustment unless NWC is more than 10% off target) around the peg, to avoid disputes over minor timing differences

- For advisors: Integrate the working capital analysis with the EV‑to‑equity bridge and QoE findings so that cash conversion, reserves, and peg methodology tell a consistent economic story from diligence through closing

Share Your Perspectives: Have you encountered a situation where reclassifying an item between NWC and debt‑like materially changed the deal economics? How did you resolve it?